Thank God for Shale Oil and Gas

We'd be fucked without it

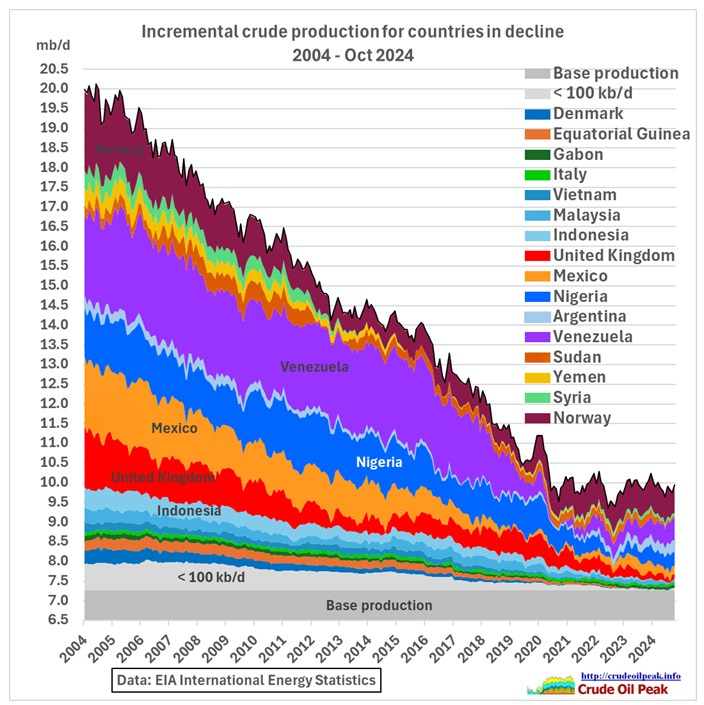

Image Source - US shale oil seems to cover up peaking crude oil production in the rest of the world since 2018

Unlike conventional oil which has a gentle decline, shale production collapses quickly once it peaks.

Shall we have an office pool to guess how long before we tip into severe enough energy deficit so as to cause the current economic contraction to mutate into a full blown collapse?

I’ll go first - maximum two more years.

Natural Resources Market Commentary - Gas Production is Declining

Goehring & Rozencwajg Natural Resource Investors

In the volatile world of U.S. natural gas, the past quarter unfolded with all the drama of a Shakespearean act. Prices began at a modest $2.60 per Mcf, buoyed by the quiet equilibrium of early spring. But by mid-June, the plot had transformed. An unseasonal heat wave gripping the central United States sent prices soaring to $3.15, a rally that spoke as much to the market’s sensitivity as it did to the hot weather. Yet, as quickly as the heat arrived, it receded. Milder temperatures reclaimed the stage and gas prices tumbled in response, bottoming at $1.90 by the end of August.

While market participants obsessed over weather patterns, few paused to consider the silent protagonist in this unfolding drama: inventories. The 2023–2024 winter, among the warmest on record, left a legacy of near-record storage levels. At the outset of the injection season, inventories stood at a staggering 700 Bcf—or 40%— above the ten-year average. Yet, tight fundamentals have nearly erased this surplus in a remarkable turn. Over the third quarter alone, inventories were drawn down by almost 400 Bcf. By quarter’s end, storage levels stood less than 5% above the norm, a quiet but profound shift that few have fully grasped.

This brings us to the present moment, where the market stands at a crossroads. If the coming winter delivers typical cold—after two years of unseasonable warmth—U.S. natural gas prices could well align with international benchmarks which currently hover near $14/MMBtu. The implications are vast, mainly as U.S. natural gas production, once seemingly boundless, now hints of rolling over.

Over the past fifteen months, growth in U.S. gas production has stalled. Indeed, in the past seven months, production has begun to contract. Since peaking in December 2023, U.S. dry gas supply has fallen by 3 Bcf per day—a 3% decline. Year-over-year data tells a similar story, with dry gas production now down by 1.2 Bcf per day, slightly more than 1%.

The natural gas bears, ever resourceful, have latched onto recent productivity data, pointing to gains in drilling efficiency across several shale plays as evidence of a potential resurgence. Yet this narrative, seductive though it may be, demands scrutiny. Our analysis, informed by deep neural networks, reveals that these productivity gains are not the herald of renewed growth but rather the predictable consequence of declining rig counts.

Consider this: in August 2022, the Baker Hughes natural gas rig count stood at 166. By February 2024, that number had dropped to 121, a 27% decline. Over the past seven months, the rig count has fallen further, reaching just 101—a 17% plunge in a remarkably short time. As every seasoned industry observer knows, exploration and production companies cut their least productive rigs first, leading to an inevitable but temporary boost in reported drilling productivity.

But this veneer of efficiency masks a more profound truth. Producers, facing dwindling options, have concentrated their remaining rigs on the final Tier 1 drilling areas within their plays. This “high-grading” of inventories explains the reported productivity gains of the past eighteen months but also signals an endgame. Our analysis suggests that Tier 1 drilling inventory in these plays is rapidly being exhausted. The accompanying graphics in this letter’s “Shale Fields and the Hubbert Curve” section lay bare this reality, using the Marcellus as a case study in depletion dynamics.

The broader picture is no less sobering. All U.S. natural gas production sources, whether from dedicated shale gas plays or associated gas from shale oil operations, are plateauing. Against this backdrop, demand is poised to surge. LNG exports are set to expand dramatically, while the data center boom adds another layer of consumption to the mix.

The result? A market that is shifting, after fifteen years of structural surplus, toward a long-running structural deficit. The abundance of shale gas has defined the natural gas story for the past decade and a half. That era, we believe, is drawing to a close, and the implications for prices—and the broader energy landscape—are profound. Read More

Meanwhile…

A 25-Percent, 24-Hour Tariff Clown Show, Trump May Roll Back Tariffs Tomorrow

The Ministry of Truth scriptwriters are working very hard on trying to eclipse Idiocracy. And then there’s the MRNA Measles Vaccine that Trump and RFK Jr are supporting.

How Does One Address a Significant Shortage of Gas?

"We took a hit for New Zealand. Meridian put this country's security of supply first and as New Zealand's largest renewable electricity generator, our balance sheet tends to underwrite the mitigation of extended droughts, and that's one of the ways the country benefits from having large and financially strong gentailers."

The company was preparing for the 2025 winter and recently signed a new agreement with the Tiwai Point aluminium smelter, which has agreed to reduce demand by 50 megawatts.

"The bigger issue, though, is the structural and significant shortage of domestic gas. New Zealand needs to take urgent action to address this.”

Energy limits are forcing the economy to contract

Energy have nots are deindustrializing… example The global economy is dying.

And last but not least, the Mass Murder continues in Brazil:

For many around the world, vaccine mandates were a looming threat—policies debated, protested, and, in some cases, resisted. But in Brazil, there is no debate. No exemptions. No alternatives. No way out. It’s crucial to recognize the stark difference between a mandate and forced compliance under duress.

In Brazil, there is no escape.

Parents who resist face harsh penalties:

Crippling fines amounting to thousands -- sometimes tens of thousands — of US dollars.

Police intimidation and threats for noncompliance.

Stripping of parental rights and loss of parental control.

Chris Martenson posted this comment on his website. It paints a clear picture at the types of investment(s) and commitments it takes to extract oil out of the ground. This is all going to end pretty much as Gail Tverberg has said that we will reach a point where oil must be sold at a minimum price and that price will be much too high for the consumer, so it stays in the ground. Michael Rupert who made the Movie Collapse was also of this belief.

-----------------------------------------------------------------------------------------------

” was just speaking yesterday with a gentleman with 40 years of experience in the oil services business. He operated all over the world, from the North sea, to the Middle East, Africa, and all over the US.

His assessment of the ANWR oil was based on having also worked there putting in man camps, delivering water and oil tanks and other services.

He said, point blank, “They could give that lease land away, and remove every possible fee or tax and it still wouldn’t get drilled. The price of oil is too low.”

Bang! There it is.

His reasoning was that there’s no infrastructure up there. No roads. No electrical lines. No pipelines. No conditioning plants. No welding shops. No restaurants. Nothing.

You have build or bring everything to the show.

By way of example, he said “Just consider the man camps, which were a focus of mine. To build out a 400 person facility is at least $15 million. That’s about what you’d need for a mid-sized operation. We can’t fly all that in, so we have to build roads. In that part of Alaska you have to hug the coasts so you have something solid under your trucks. Alternatively you have to wait for the right temperatures and then build ice roads. Depending on condtions and topography those costs range from heavy to extreme. So who pays for that? If you’re asking my company to do that, and we did, we need contracts that both cover our costs and reasonable profits. At a minimum those are 5 year contracts. After Biden, who is going to sign a 5-year contract to build something that might be zeroed out by the next administration?”

We are burning the industrial civilization (IC ) candle at both ends: through the artificial man made construct of debt and through the natural laws of physical thermodynamics of energy cost of energy (ECoE) / energy returned on energy invested (EROEI).

Producing oil coal or NG is a complex specialized task that requires a form of money as a medium of exchange to coordinate drilling , refining, maintenance, and transport.

When the financial system crashes, then so does the specialized interconnected industry needed for extracting energy. When it costs more energy to get that barrel of oil out of the ground than that same barrel provides, then the system also crashes.

Debt and physics. Either way.